A systematic trading approach is a predefined, rule-based methodology where every trading decision follows objective criteria established before a position is opened. Entry signals, exit conditions, position sizing, and risk limits are all defined in advance, removing emotional judgment from execution. This structure is what separates systematic trading from discretionary trading, where a trader's gut, experience, or real-time interpretation drives decisions. Systematic trading now accounts for a majority of total volume on major global equity and derivatives exchanges. That shift reflects how thoroughly the industry has moved toward data-driven execution over human intuition.

What rules and criteria define a systematic trading approach?

A systematic trading approach is defined by four core rule categories: entry signals, exit conditions, position sizing, and risk management limits. Each category uses quantifiable data and predefined parameters, not discretion. Explicit predefinition removes loss aversion and FOMO by replacing emotional triggers with objective rules. That means a trader never decides "this feels right." The system either fires a signal or it does not.

Common rule categories in systematic strategies

- Entry signals: Price crossing a moving average, RSI reaching an oversold threshold, or a breakout above a defined resistance level.

- Exit conditions: A fixed profit target, a trailing stop, or a time-based exit after a set number of bars.

- Position sizing: A fixed percentage of capital per trade, or a volatility-adjusted formula such as the ATR-based method.

- Risk limits: Maximum drawdown thresholds, daily loss caps, and correlation limits across open positions.

The three most common strategy archetypes are momentum, mean reversion, and statistical arbitrage. Momentum strategies buy assets trending upward and sell those trending down. Mean reversion strategies bet that prices will return to a historical average after an extreme move. Statistical arbitrage exploits pricing inefficiencies between related instruments using quantitative models. Each archetype uses a different signal logic, but all three share the same structural discipline: rules first, execution second.

Risk is controlled programmatically within the system itself. The 3-5-7 rule defines maximum thresholds for individual trade risk, total open exposure, and overall capital at risk. That framework gives traders a concrete starting point for building risk limits into their rulebook before they ever place a live trade.

Pro Tip: Write your rules in plain language before coding them. If you cannot explain your entry signal in one sentence, the rule is too vague to trade systematically.

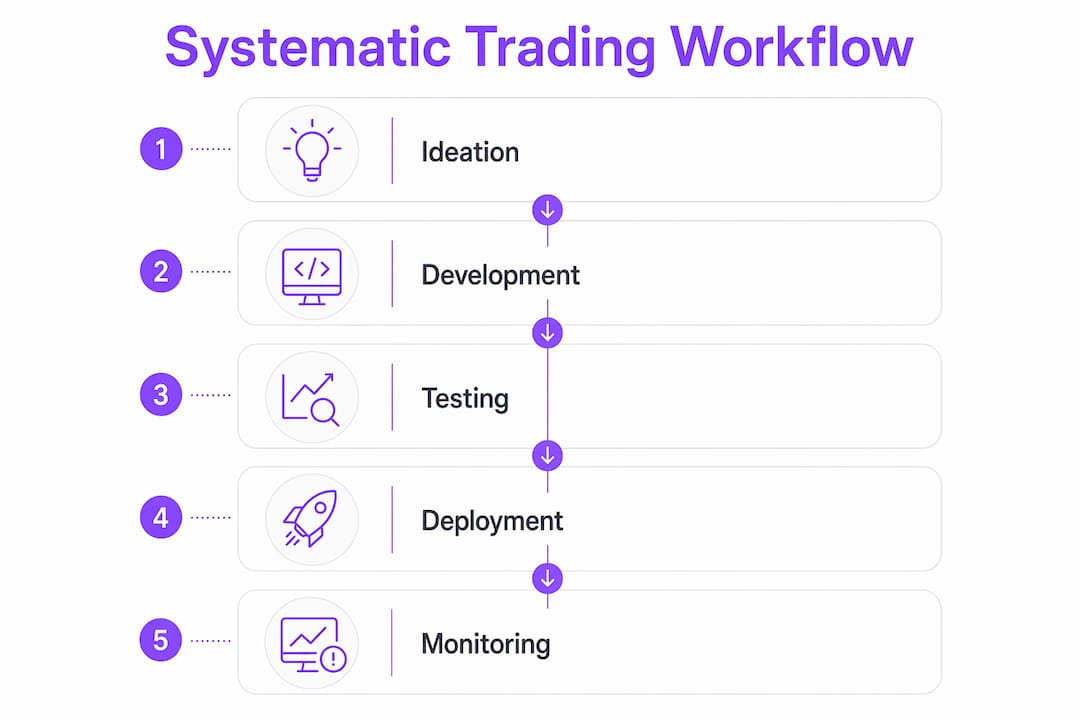

How is a systematic trading approach developed and tested?

Strategy development follows a four-stage process. Skipping any stage increases the probability of deploying a system that works on paper but fails in live markets.

- Strategy ideation: Define the market hypothesis. What inefficiency are you exploiting? Why should it persist? A momentum strategy, for example, assumes that assets with recent price strength will continue outperforming in the near term.

- Rigorous backtesting: Apply the rules to historical data and measure performance metrics including win rate, average win-to-loss ratio, maximum drawdown, and Sharpe ratio. Backtesting must include realistic trading costs and slippage to avoid overfitting. A strategy that looks profitable before costs often fails after them.

- Walk-forward validation: Divide historical data into in-sample (used to build the rules) and out-of-sample periods (used to test them). Walk-forward testing checks whether the strategy generalizes beyond the data it was built on. This step directly addresses curve-fitting risk.

- Live deployment with documented logs: Trade the system with real capital under defined risk controls. Maintain a detailed trade log for every signal, execution, and outcome.

| Development stage | Primary risk | Key action |

|---|---|---|

| Ideation | Confirmation bias | Define hypothesis before testing |

| Backtesting | Overfitting to history | Include costs and slippage |

| Walk-forward validation | Curve fitting | Use out-of-sample data |

| Live deployment | System drift | Monitor and log every trade |

The four-stage workflow is the industry standard for systematic strategy deployment. Each stage builds on the previous one, and the documented trade log created in stage four becomes the foundation for ongoing performance reviews.

Pro Tip: Never optimize a strategy on the same data you used to build it. Reserve at least 30% of your historical data as a clean out-of-sample test set before you run a single optimization.

What are the key advantages and limitations of systematic trading?

Systematic trading eliminates emotional bias by design. A trader who follows a rulebook cannot revenge trade after a loss or hold a winner too long out of greed. That structural discipline is the primary advantage, and it compounds over time. Systematic trading's greatest edge is consistent discipline and scalability across markets, something a discretionary trader cannot replicate manually across dozens of instruments simultaneously.

Benefits of systematic trading

- Consistency: The same rules apply in every market condition, removing the variability that comes from mood, fatigue, or overconfidence.

- Scalability: One rulebook can govern positions across multiple markets, timeframes, and asset classes at once.

- Transparency: Every trade has a documented reason. Post-trade reviews become straightforward because the decision logic is already written down.

- Speed: Automated execution removes the delay between signal and order, which matters in liquid, fast-moving markets.

- Emotional protection: Traders who struggle with emotional trading get a structural barrier between their feelings and their orders.

Limitations to understand before you start

Systematic trading is not without real challenges. Curve fitting is the most common failure mode. A strategy optimized too tightly to historical data will look excellent in backtesting and collapse in live trading. Ongoing oversight is non-negotiable. Systematic trading requires active monitoring to maintain performance, not a set-and-forget mindset. The initial complexity of building, testing, and validating a system also creates a real barrier for newer traders.

One critical misconception is that systematic trading requires high-frequency algorithms and expensive infrastructure. Manual adherence to a predefined rulebook is equally systematic as full automation. The defining criterion is that two traders using the same system would execute identical trades based on the same objective rules. Speed and technology level are secondary.

How can traders practically use systematic trading to improve discipline?

Applying a systematic approach in practice starts with strict adherence to the written rulebook, even when the market "feels" different. The moment a trader overrides a signal based on intuition, the system's statistical edge begins to erode. Post-trade reviews detect system drift early, before a performance deviation becomes a serious drawdown.

Practical steps for traders building systematic discipline:

- Document every trade: Record the signal, the entry price, the exit price, and whether the trade followed the rules exactly. Deviations are data points, not just mistakes.

- Set hard risk limits before each session: Define your maximum loss for the day and the maximum position size before markets open. Remove the decision from the heat of trading.

- Schedule weekly system reviews: Compare live results to backtested expectations. A consistent gap signals either system drift or execution error.

- Use market replay to practice: Replaying historical price action under your rules builds pattern recognition without risking capital. This is especially useful for traders new to a strategy archetype.

- Incorporate AI-assisted trade auditing: AI in trading psychology now identifies behavioral patterns like revenge trading and FOMO in real time, giving traders objective feedback on execution quality.

Risk management belongs inside the system, not as an afterthought. Position sizing rules, stop-loss levels, and daily loss caps are not optional add-ons. They are core components of the rulebook. A systematic approach without embedded risk controls is not systematic. It is just a trading idea with no guardrails.

Pro Tip: Track your rule adherence rate separately from your profit and loss. A trader who follows the rules and loses is getting useful data. A trader who breaks the rules and wins is building a dangerous habit.

Key Takeaways

A systematic trading approach works because it replaces emotional judgment with objective, predefined rules that apply consistently across every trade, market, and condition.

| Point | Details |

|---|---|

| Rule-based execution | Define entry, exit, sizing, and risk limits before placing any trade. |

| Four-stage development | Ideation, backtesting, walk-forward validation, and live deployment with logs. |

| Not always automated | Manual rule-following is equally systematic as algorithmic execution. |

| Active oversight required | Monitor for system drift and adapt when live results diverge from backtested results. |

| Discipline is the edge | Consistent rule adherence, not prediction, is what separates systematic traders over time. |

What I have learned from years of watching traders go systematic

Most traders who fail at systematic trading do not fail because their rules are wrong. They fail because they stop following the rules the moment the system hits a losing streak. That is the real test of a systematic approach, and it is a psychological test, not a technical one.

The second most common mistake I see is building a strategy that looks perfect on historical data. Traders spend weeks optimizing parameters until the backtest equity curve looks like a straight line going up. Then they go live and the system falls apart within two months. Confirmation bias during system design is the culprit. Traders unconsciously select the data and parameters that confirm what they already want to believe.

The fix is not more sophisticated math. It is intellectual honesty. Build the simplest version of your hypothesis first. Test it on data you have never looked at. If it holds up, add complexity. If it does not, the hypothesis was wrong, and you saved yourself real money finding out cheaply.

One more thing worth saying clearly: systematic does not mean slow or boring. Slow systematic strategies on longer timeframes are just as valid as high-frequency models. A weekly mean reversion system on equity indices requires the same discipline as a millisecond arbitrage algorithm. The timeframe changes. The commitment to the rules does not.

— Tony

How Disciplineaiapp supports your systematic trading practice

Disciplineaiapp is built for traders who understand the rules but struggle to follow them consistently under pressure.

The platform combines AI analytics with behavioral coaching to audit every trade against your predefined rules. Its automated trade auditing feature flags deviations in real time, so you know immediately when emotion has overridden your system. The market replay feature lets you practice your rulebook on historical data before risking live capital, which is the closest thing to a flight simulator that systematic traders have. Disciplineaiapp also tracks emotional patterns like revenge trading and FOMO across your trade history, giving you the behavioral data you need to close the gap between your system's edge and your actual execution. Explore the full AI trading platform to see how it fits your strategy.

FAQ

What is the systematic trading definition?

A systematic trading approach is a rule-based methodology where entry, exit, position sizing, and risk management criteria are defined in advance to remove emotional bias from every trading decision.

How does systematic trading differ from discretionary trading?

Systematic trading follows a fixed rulebook applied identically in every situation. Discretionary trading relies on a trader's real-time judgment, experience, and interpretation of market conditions.

Does systematic trading require automation?

No. Systematic trading can be manual or fully automated. The defining criterion is that two traders using the same system would execute identical trades based on the same objective rules, regardless of technology level.

What is the biggest risk in systematic trading?

Curve fitting is the primary risk. Over-optimizing a strategy to historical data produces a system that performs well in backtesting but fails in live markets because the patterns it learned do not repeat.

What is the 3-5-7 rule in systematic trading?

The 3-5-7 rule defines maximum thresholds for individual trade risk, total open exposure, and overall capital at risk. It gives systematic traders a concrete framework for building position sizing and risk limits into their rulebook.